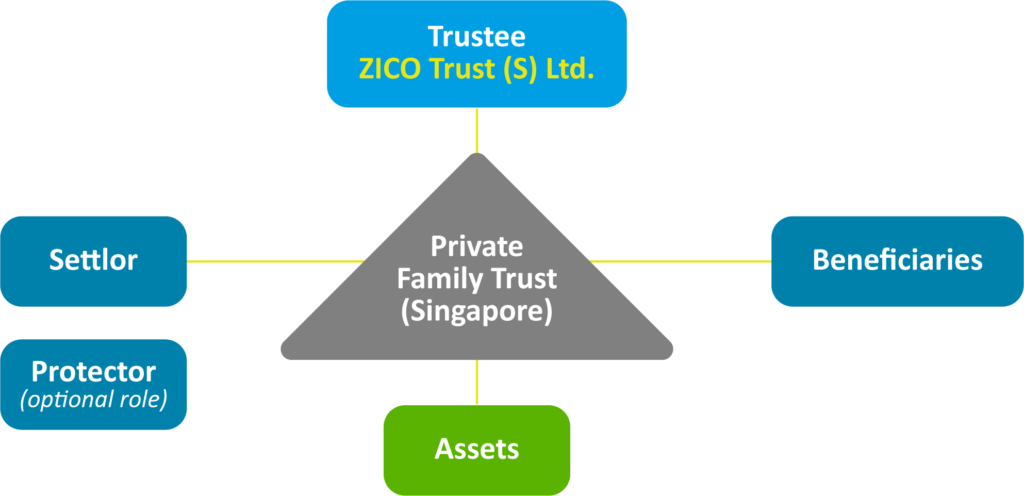

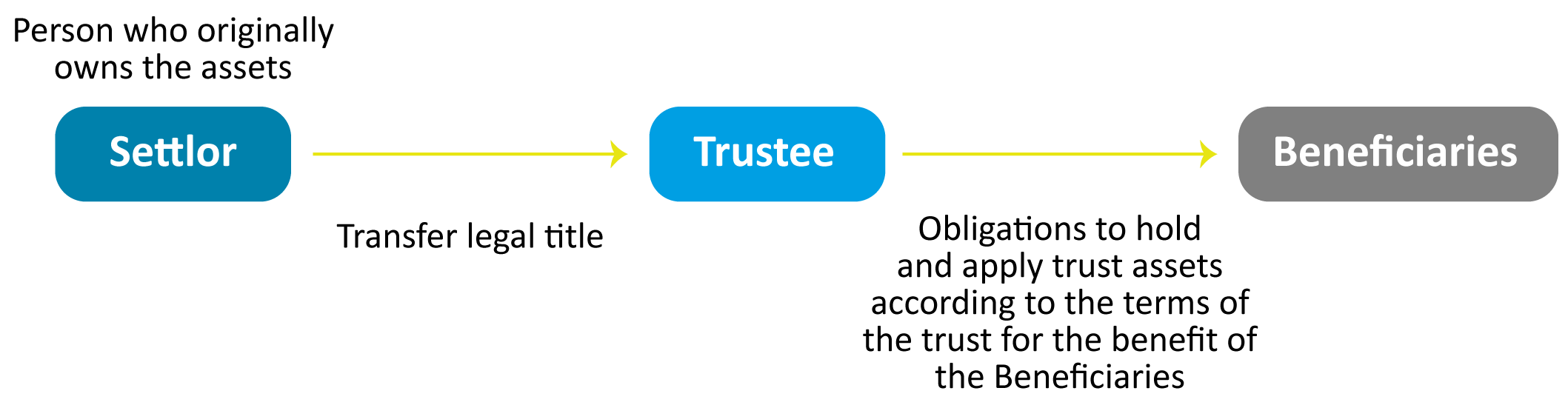

A trust is a legal arrangement whereby the ownership of a property is divided between two parties, such that one person is entrusted with the legal title to the property (the trustee) whilst another person (the beneficiary) retains the beneficial (or equitable) ownership of the property. The original owner of the property who creates the trust arrangement (the Settlor) would enter into this arrangement in order to allow the trustee the control to manage and administer the property, whilst being assured the economic benefits from the property will accrue to the beneficiary.

A private family trust is usually designed to help a high net-worth individual preserve assets and facilitate the transfer of assets to future generations. Trusts provide continuity in the administration of assets, especially if a company (as opposed to a specific individual) is chosen as the trustee. A properly setup trust ensures protection of assets and can provide continuity of benefits to family members across generations.